Why are ESG research houses losing senior staff and making redundancies?

Exclusive: After Sustainalytics, companies including MSCI and ESG Book have also been shedding c-suite and research staff, often without announcement. What are the implications?

Morningstar’s announcement in September last year that it was laying off 10% of the global headcount at Sustainalytics, its ESG research subsidiary, was a stark indicator that the ESG pushback in the US was hitting the bottom line.

It was all the more surprising because it had followed a recruitment boom at Sustainalytics in the preceding years as the ESG regulatory environment hardened under the European Union’s (EU) Sustainable Finance Disclosure Regime (SFDR) for investors.

I can reveal that Sustainalytics hasn’t been the only ESG research house letting people go or leaking senior staff as times get harder.

MSCI, the market leader in ESG research, where it jockeys for the top spot with Sustainalytics, has also quietly been trimming numbers, according to insiders.

Sources within MSCI say there was a drip-feed of redundancies across its ESG and climate teams last year. They say that a number of the US ESG and climate coverage team was laid off during 2023, alongside some senior ESG team heads, following a sharp focus on cost reduction after lower than expected target results.

In terms of the senior head departures, Edward Allen, Managing Director, Head of Americas Client Coverage for ESG and Climate Research was made redundant towards the end of last year, without a public announcement. Allen had been with MSCI for 20 years and spent the last five and a half years building up a 75-plus person team in New York.

Shortly after that, his London-based counterpart responsible for MSCI’s largest ESG&C client region, Jillis Herpers, Managing Director, Head of EMEA Environmental, Social and Governance (ESG) & Climate - Client Coverage - another almost 20-year MSCI employee - was also made redundant, again without public announcement. Herpers oversaw a team of nearly 100 people.

The sources say the two senior redundancies caused significant disturbance within MSCI’s ESG and Climate division.

MSCI came under attack at the beginning of the year from hedge fund, Spruce Capital, which went public with its short position in the firm. One of the four main reasons for shorting the stock, Spruce said, was that: “Despite having been MSCI’s recent growth driver, the Company’s ESG and Climate segment is now beginning to struggle.”

MSCI told me it categorically refutes the claims made by Spruce Capital.

But MSCI’s share price was certainly rocked concurrent to the attack. It dropped from $602.24 on Jan 31 to $446 by April 23. It has since recovered to $490.50 as of June 3.

The share price has more than doubled over the past five years, however.

Regarding its staff levels and departures, MSCI told me: Our employee turnover rate is very low, at under 5%. Per our policy we don’t comment on employee departures.”

It is not only the big ESG players that have taken a hit.

ESG Book, the Frankfurt-registered data and research provider that bagged $35m of investor funding in June 2022 - notably from Energy Impact Partners (EIP), a New York-based private equity fund run by Hans Kobler, its German founder and managing partner - has been steadily losing members of its c-suite.

Leon Saunders Calvert, chief product officer, announced that he had left the firm in April after only 19 months, following CEO Daniel Klier’s surprise departure at the end of February.

ESG Book did not disclose, however, that its chairman, John Wise, a well-known tech entrepreneur based in Santa Monica, California, had also left the company’s board after just six months, having joined it in October 2023.

And a number of top personnel had already exited ESG Book in the previous 13 months without announcement.

The firm’s global head of research, Todd Arthur Bridges - a former head of ESG research at State Street Global Advisors - left in summer 2023. Alessandro Pavone, global head of sales, left in February 2023 after just over two years in post.

I understand that ESG Book is not directly replacing the senior staff that have left, with the exception of Klier, due to internal restructuring.

Klier had been CEO for almost three years when he unexpectedly quit at the end of February, and last month joined South Pole, the carbon markets and climate advisor, as CEO.

Klier’s shift away from ESG research to climate data is interesting. I’ll come back to this shortly.

A spokesman for ESG Book said Klier’s replacement was being sought: “A process is currently underway to identify the best long-term candidate for the role of CEO.”

ESG Book had not responded to a request for comment by the time of writing on whether a replacement for Klier had been found.

Klier was leading ESG Book at the time of the Series B funding round in 2022. Investments into ESG Book were also made by Meridiam, the French infrastructure fund manager, and Allianz X, the digital investments arm of the German insurance giant.

ESG Book has been investing in staff though. Reported numbers in 2021 had reached 56. The company says it now employs more than 200 people globally, with most based in Frankfurt and London.

But so far, ESG Book, which was formerly known as Arabesque S-Ray, has not reported a profit.

The latest available financial accounts in Germany show that ESG Book made a loss in 2021 of €5.9m, following a €7m loss in 2020. Turnover was up over the same year, estimated at €21m in 2021 against €18m in 2020.

A spokesperson for ESG Book said the company had grown in 2022: “As an indication of the company's growth in that year, ESG Book's annual recurring revenue grew by over 2.5x, with gross margin increasing to over 70 percent.”

But a source close to the company said it had been facing a contraction in the research market coupled with “brutal competition” in the ESG data sector.

I started this piece with the Sustainalytics lay-offs from last September.

Subsequent to that announcement, it has also lost top staff. Bob Mann, its President & Chief Operating Officer left the company in March this year. He joined Glass Lewis, the proxy voting advisor, as CEO.

Ron Bundy, President, Morningstar Sustainalytics & Morningstar Indexes, is understood to be on the lookout for a replacement to lead that business.

There was also quite a bit of turnover in Moody’s ESG Solutions business in early 2023 with a number of former Vigeo senior team members including Michael Notat, Head of Global Sales Strategy and Julia Haake, Managing Director, Market Strategy, leaving the firm. Moody’s bought a majority stake in Vigeo-Eiris in 2019.

So what’s going on in ESG research that’s making times tougher? And why should we care?

Taking the second point first: a high quality data and research sector is important to ESG. It indicates that investors are willing to pay for material sustainability inputs alongside financial considerations when investing in companies.

On the first point, ESG research professionals say the reason for the downturn is that investor client budgets for ESG data have gone down while timelines for buying decisions have become much longer.

They say the US anti-woke ESG pushback has had a big impact; it is no surprise that the big players that have clipped headcount are both US companies.

The EU’s regulation introduced in April this year on transparency of ESG research firms is undoubtedly playing a part also, given that one major rule is that it requires giving companies a right to review and correct data used in ESG ratings that the company deems factually incorrect.

I’ll come back to these regs in another piece, as I think they’re important, and will certainly impact the ESG research market.

There’s also the potential for AI to replace analysts in a field where the top-down regulatory/incentives pressure that would make ESG data clearly valuable financial analysis are still relatively weak.

The bumper years of the early 20s have waned. Insiders say SFDR advisory and reporting work had been a boon at the beginning of the decade, but have become less important as the regulation beds in.

The ESG research market is also relatively mature and well served. This means business revenues flatten with fewer new market entrants.

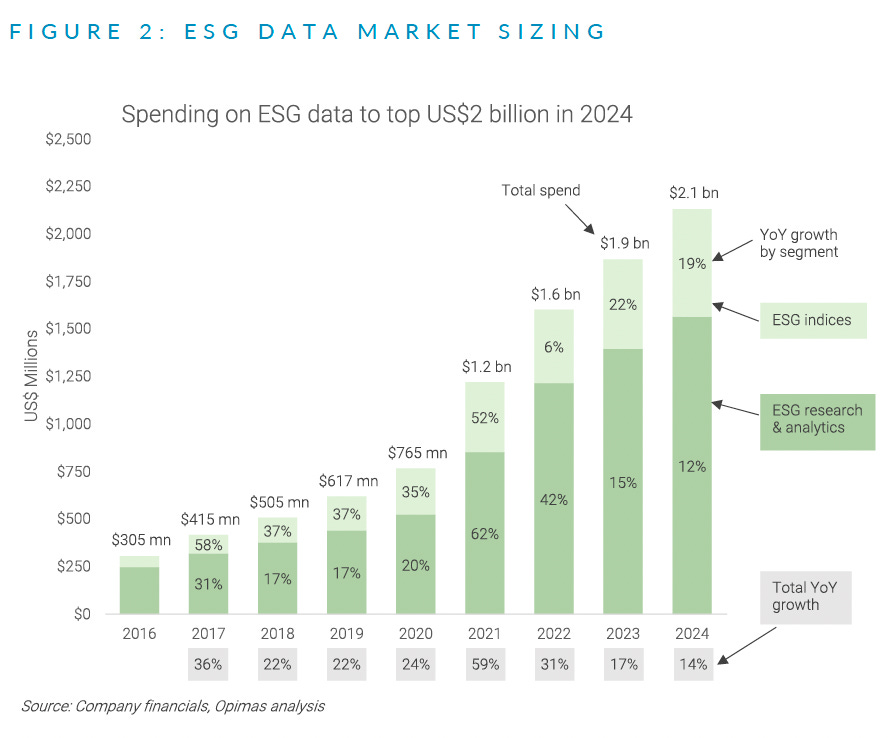

A report published earlier this month by Opimas, the management consultant, says the year-on-year market growth rate for ESG data slowed in 2023 to 17 percent from 42 percent in 2022. Growth is likely to slow again this year to 14 percent, according to the report.

Nevertheless, in the report, titled The Market for ESG Data in 2024, Opimas expects spending on ESG data to exceed US$2 billion in 2024, up from nearly half that amount in 2021.

Climate data, however, is potentially a more interesting growth market given focus on net zero targets and energy transition data for companies and investors. As a result, it is also more competitive.

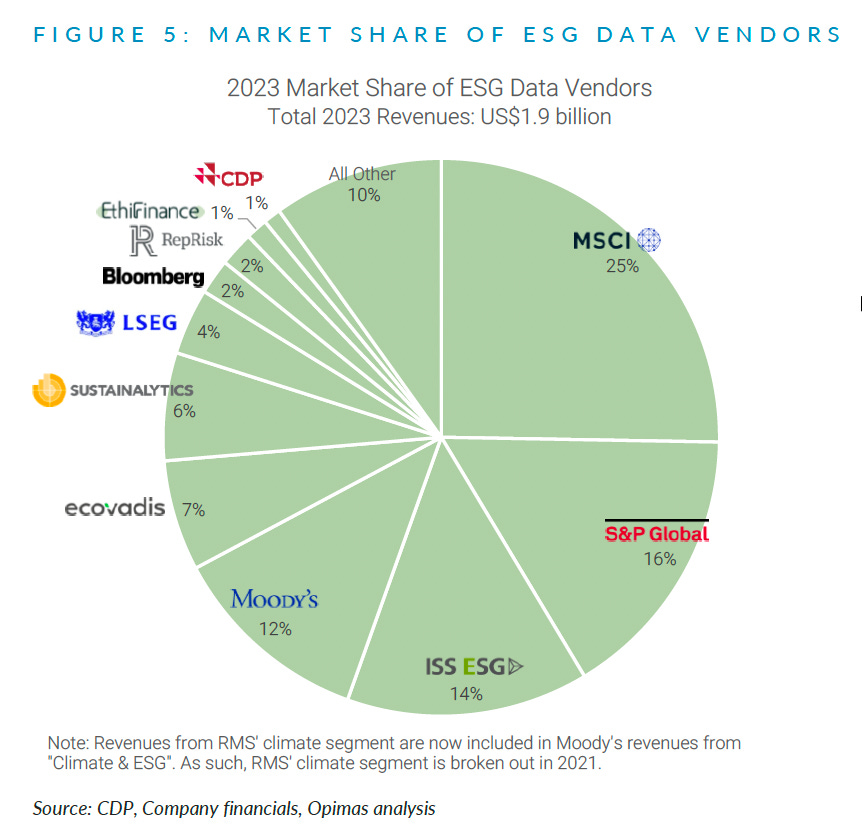

S&P Trucost is believed to be the biggest player in the climate data market, and MSCI jostles with other big players such as Moody’s and ISS.

Consequently, there has been more recent joint-venture and M&A activity.

S&P Trucost partnered with Oliver Wyman, the management consultant, in 2021 to launch Climate Credit Analytics for climate risk regarding the debt at public and private companies.

BlackRock, the funds giant, bought Baringa Partners’ Climate Change Scenario Model in 2021 to integrate into its Aladdin data platform.

MSCI recently bought UK-based carbon analytics company Trove Research.

The number of start-up and growth players has also grown with the likes of Clarity AI coming to market joining growth companies in the field like Persefoni and GIST Impact

Investment is required to scale climate data businesses, but the market is also tight in terms of revenues.

Some think that biodiversity data under the Taskforce for Nature-Related Financial Disclosure and related initiatives could be a growth spurt. But that’s another topic for a future piece.

Hugh - nice job and great to see you resurface with some solid journalism! I think regulation will play a huge role in redefining ESG >>> sustainability data away from nice to have and people with a passion to a professional class with highly specified knowledge. It will align more with existing practice in environmental protection, health and safety regulations. This means that "ESG" research will change significantly from high level platitudes to more technical issues, risk assessment and the realities of trade-offs companies have to make. Mandated data will remove much of the "competitive advantage" gained in the past years by ESG data providers from capturing (often manually) ESG data. CFAs and CPAs will have to move aside and let those with technical training in the wide range of sustainability risks take over and ensure compliant auditable data. CPAs can at best make sure reporting processes are functional, but cannot provide subject matter expertise.

This will take a few years, and ISSB will attempt to fill the void until national financial regulators set their own specified rules.

Great piece huge, well done! My understanding is that the current shrinkage in the sector could also be partly due to optimistic overexpansion over the past five years. I think the pendulum is just swinging back the other way and will eventually reach equilibrium, which could be a healthy outcome overall. Prospective regulation of ESG data and rating providers is also taking its toll.